January 2023 - Market Commentary

4Q 2022 Recap & 1Q 2023 Outlook

Recapping A Challenging 2022

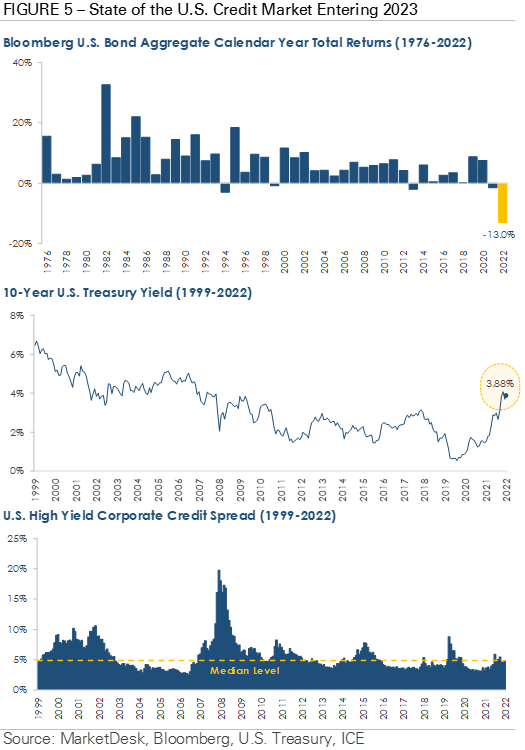

Markets faced several challenges in 2022, including high inflation, historic central bank policy, the war in Ukraine, and Covid lockdowns in China. Inflation was a major factor in the markets throughout the year, with the headline consumer price index reaching a 40-year high of 9.1% in June. High inflation prompted the Federal Reserve and its global central bank peers to aggressively raise interest rates, which caused stocks and bonds to trade lower. There was no place to hide as central banks rapidly tightened monetary policy. Figure 1 shows the S&P 500 returned -19.4% in 2022, its worst annual return since 2008, and Figure 5 shows the Bloomberg U.S. Bond Aggregate produced its worst total return since 1976. This letter reviews the fourth quarter, recaps a difficult 2022, and discusses what the market will be focused on in 2023.

Putting 2022’s Interest Rate Hikes Into Perspective

The main story of 2022 was the reversal of monetary policy from extraordinarily accommodative levels during the Covid-19 pandemic. Figure 2 shows the speed and size of interest rate increases as central banks worked to bring inflation under control. The chart tracks the cumulative percentage of interest rate increases and decreases by global central banks during rolling three-month periods since 1995. For example, the 68% at the end of November 2022 indicates that central banks across the globe raised interest rates by a total of 68% from September to November. In contrast, the total amount of interest rate cuts during that same period was only 4%. As the data shows, 2022 was the quickest, largest, and most imbalanced global tightening cycle since the late 1990s.

The pace of interest rate increases is forecasted to slow during 2023. Central banks continue to hint that they are approaching the end of their interest rate hike cycle, citing concerns that further tightening could push the economy into recession. In addition, data suggests price pressures are easing. While the year-over-year headline consumer price index rose by 7.1% in November 2022, which is still high compared to historical levels, it was down from the 9.1% rate seen in June 2022. As inflation and central bank policy return to normal, a new uncertainty is emerging – the unknown effects of 2022’s rate hikes.

Markets Wait for the Lagged Effect of Higher Interest Rates to Show Up in Economic Data

The Federal Reserve's interest rate hikes occurred in 2022, but the full impact of its restrictive measures has not yet been fully felt in the real economy. While the U.S. economy contracted during the first half of 2022, it expanded at a robust +3.2% annualized pace during the third quarter. Consumer spending remained strong throughout most of 2022 despite high inflation, and the U.S. labor market added more than 4 million jobs through the end of November. The data indicates the U.S. economy has withstood tightening thus far, but the real test will come in 2023 as the cumulative impact of higher interest rates becomes clearer.

While a recession is not a foregone conclusion, it is possible the economy could be tested in 2023. An index of leading economic indicators shows the U.S. economy is already starting to slow as the impact of higher interest rates takes hold. Figure 3 graphs the month-over-month change in The Conference Board's Leading Economic Index, which tracks ten economic components that tend to precede changes in the overall economy.

Included in the components are the average weekly hours worked by manufacturing workers, new home building permits, and the volume of new orders for capital goods, such as equipment, vehicles, and machinery. The chart reveals that the Leading Economic Index has decreased every month since March 2022, an indication the economy is slowing after a period of strong growth during the pandemic recovery.

Equity Valuations Are More Attractive, But Corporate Earnings Are An Open Question

Whereas inflation and central bank policy were the primary drivers of markets in 2022, economic data and corporate fundamentals are expected to play a larger role in determining the market’s direction in 2023. Figure 4 tracks two important S&P 500 metrics. The top chart tracks the next 12-month price-to-earnings ratio, which divides the S&P 500’s projected next 12-month earnings by its current price. It shows valuation multiples expanded during the pandemic as interest rates were cut to near 0% before reversing lower during 2022 as rising interest rates weighed on company valuations.

While current valuations are at a more attractive starting point today than at the beginning of 2022, corporate earnings are an open question entering 2023 with the potential for an earnings reset as the economy slows. The bottom chart in Figure 4 tracks the S&P 500’s trailing 12-month earnings growth, showing the jump in corporate earnings during the pandemic. Despite expectations for an economic slowdown, Wall Street analysts still forecast single-digit earnings growth for the S&P 500 in 2023. The positive earnings growth forecast is encouraging, but it creates a risk for the market. If actual earnings growth falls short of the forecast, stock prices could decline as markets price in lower actual earnings.

Equity Market Recap – Stocks Trade Higher in 4Q’22

Stocks traded lower during December but still ended the fourth quarter higher. The S&P 500 Index of large cap stocks returned +7.6% during the fourth quarter, outperforming the Russell 2000 Index’s +6.2% return. The Dow Jones Index, which includes large companies such as Visa, Caterpillar, Nike, and Boeing, was the top performer, returning +15.9%, while the Nasdaq 100 Index of technology and other growth-style stocks produced a -0.1% return during the fourth quarter.

Energy was the top performing S&P 500 sector during the fourth quarter, followed by the cyclical sector trio of Industrials, Materials, and Financials. Defensive sectors, including Health Care, Consumer Staples, and Utilities, were middle of the pack performers. Growth-style sectors, including Technology, Communication Services, and Consumer Discretionary, and interest-rate sensitive Real Estate underperformed as higher interest rates continued to weigh on valuation multiples.

International stocks outperformed U.S. stocks during the fourth quarter. The MSCI EAFE Index of developed market stocks returned +17.7% during the fourth quarter, while the MSCI Emerging Market Index returned +10.3%.

A weaker U.S. dollar boosted the returns of international stocks, with U.S. dollar weakness driven by a shrinking monetary policy gap as other central banks catch up with the Federal Reserve’s aggressive policy. Separately, China’s decision to relax its Covid-zero restrictions raised the prospect of stronger global growth as one of the world’s biggest economies reopens.

Bond Market Recap – The Great 2022 Yield Reset

The bond market experienced a significant resetting of interest rates during 2022, with yields steadily rising as the Federal Reserve pushed through large interest rate hikes. Despite posting positive returns during the fourth quarter, bonds produced significant losses during 2022 as central banks raised interest rates at a rapid pace. The top chart in Figure 5 shows the Bloomberg U.S. Bond Aggregate produced a -13% total return during 2022, its biggest negative total return since tracking began in 1976.

The bottom two charts in Figure 5 examine the current state of the credit market after 2022’s rate hikes. The middle chart shows the 10-year Treasury yield sits at its highest level since 2007. Yields are now higher across most credit classes, and investors can earn a yield of around 4% to 5% on a portfolio of high-quality bonds, such as U.S. Treasury bonds and investment grade corporate bonds, without locking up capital for long periods of time. In the corporate credit market, the bottom chart shows the high-yield corporate bond spread, which is the extra yield investors demand to loan to lower quality borrowers, is in line with its median since 1999.

The starting point for bonds, both in terms of yield and credit spreads, is now more compelling than it has been in a long time. However, there is still the potential for continued volatility in the bond market. There is still significant uncertainty regarding how high the Fed will need to raise interest rates and how long it will need to keep interest rates at restrictive levels to bring inflation down to normal levels. There is a risk that inflation could remain above the Fed's 2% target, leading to an extended tightening cycle. At the same time, the economy is likely to start feeling the effects of 2022’s rate hikes in 2023, which could make bonds more attractive. The crosscurrents of uncertain central bank policy and a volatile global economy could keep interest rate volatility elevated and test bond investors’ nerves again during 2023.

2023 Outlook – Turning the Page on 2022’s Historic Tightening Cycle

2023 brings the next phase of the tightening cycle where the lagged effects of tighter monetary policy will be felt. It has the potential to be a year of two halves. In the first half, the focus is likely to shift from the number of future interest rate hikes to how much those interest rate hikes will slow the economy. Some data, such as the housing market, indicate that tighter monetary policy is being transmitted into the economy at a rapid pace. Home sales are slowing, and homebuilder confidence weakened every month during 2022 and now sits at its lowest level since 2012. At the same time, consumers continue to spend, and employers continue to add jobs. There is still a wide range of possible outcomes, and the unique nature of the pandemic followed by rapid interest rate cuts and hikes makes the path forward less certain.

The second half has the potential to be different depending on how severe the slowdown is in early 2023. Markets are based on forward-looking decisions, and investors will be watching closely for signs that the economy has bottomed and is recovering. Plus, Figure 1 contains an encouraging historical trend. The chart shows there have only been two instances of consecutive negative S&P 500 return years since 1950, in 1973-1974 and 2000-2002. This does not necessarily mean the S&P 500 will produce a positive return in 2023 or trade higher in a straight line from here, because it may not. However, it does provide helpful historical context in a volatile environment.

Wishing you and your family happiness and health in the New Year! We look forward to serving you another year.

Source: Market Desk

SEC Registration does not imply a certain level of skill or training.

The information provided herein is for general informational purposes only and is intended for your personal use and should not be circulated to any other person without our permission and any use, distribution, or duplication by anyone other than the recipient is prohibited. No portion of this commentary is to be construed as an offer or solicitation to buy or sell a security, or the rendering of personalized investment advice. The views and strategies described herein may not be suitable for all investors and are subject to investment risks. The content is developed from sources believed to be providing accurate information. The information contained herein should not be relied upon in isolation for the purpose of making any investment decision.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation and conducted reasonable due diligence to ensure the third parties’ performance is not materially inflated or incorrect; however, we do not represent or warrant its accuracy, reliability, or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. We do not make any representation or warranty regarding any computations, graphs, tables, diagrams, or commentary in this material which are provided for illustration/ reference purposes only. These views, opinions, estimates, and strategies expressed in it constitute our judgement based on current market conditions and are subject to change without notice. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Investors may get back less than they invested, and past performance is not a reliable indicator of future results.

Data which may be found in this document is based on our research and should not be taken as a forecast or an estimate of likely future returns. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made.

Investments involve some sort of risk including potential loss of principal; diversification alone cannot guarantee against loss. Any projected results and risks are based solely on hypothetical examples depicted. Forward-looking statements should not be considered guarantees or predictions of future events. More complete information is available, including product profiles, which discuss risks, benefits, liquidity, and other matters of interest. The value of any investment may fluctuate as a result of market changes. Past performance is no guarantee of future results, and there can be no assurance the investment strategies discussed herein will prove profitable.

All opinions, estimates, investment strategies and views expressed in this document are subject to change without notice information. The recommendations made for your customized portfolio may differ from any asset allocation or strategies outlined in this document. Benchmark Financial does not guarantee the future performance of any portfolio, guarantee any specific level of performance, or guarantee any strategy or overall management will be successful or that the client’s investment objectives will be met.

Benchmark Financial is not a broker dealer and does not offer tax or legal advice. Please consult your tax or legal advisor for assistance regarding your individual situation. Investment Advisory Services offered through Benchmark Financial Wealth Advisors LLC, an SEC Registered Investment Advisor. Insurance services offered through Benchmark Financial Insurance Advisors LLC. The Benchmark Financial Wealth Advisors ADV Form 2A, 2B & Form CRS, which describe the services offered, fees charged and any conflicts of interest, are available upon request or online at www.bfllc.com. Additional information about Benchmark Financial and our advisors is also available online at www.adviserinfo.sec.gov.