June 2026- Market Commentary

Date: June 2026

From: Investment Committee

Subject: Market commentary

______________________________________________________________________

AI and Geopolitics Continue to Drive Markets

Monthly Market Summary

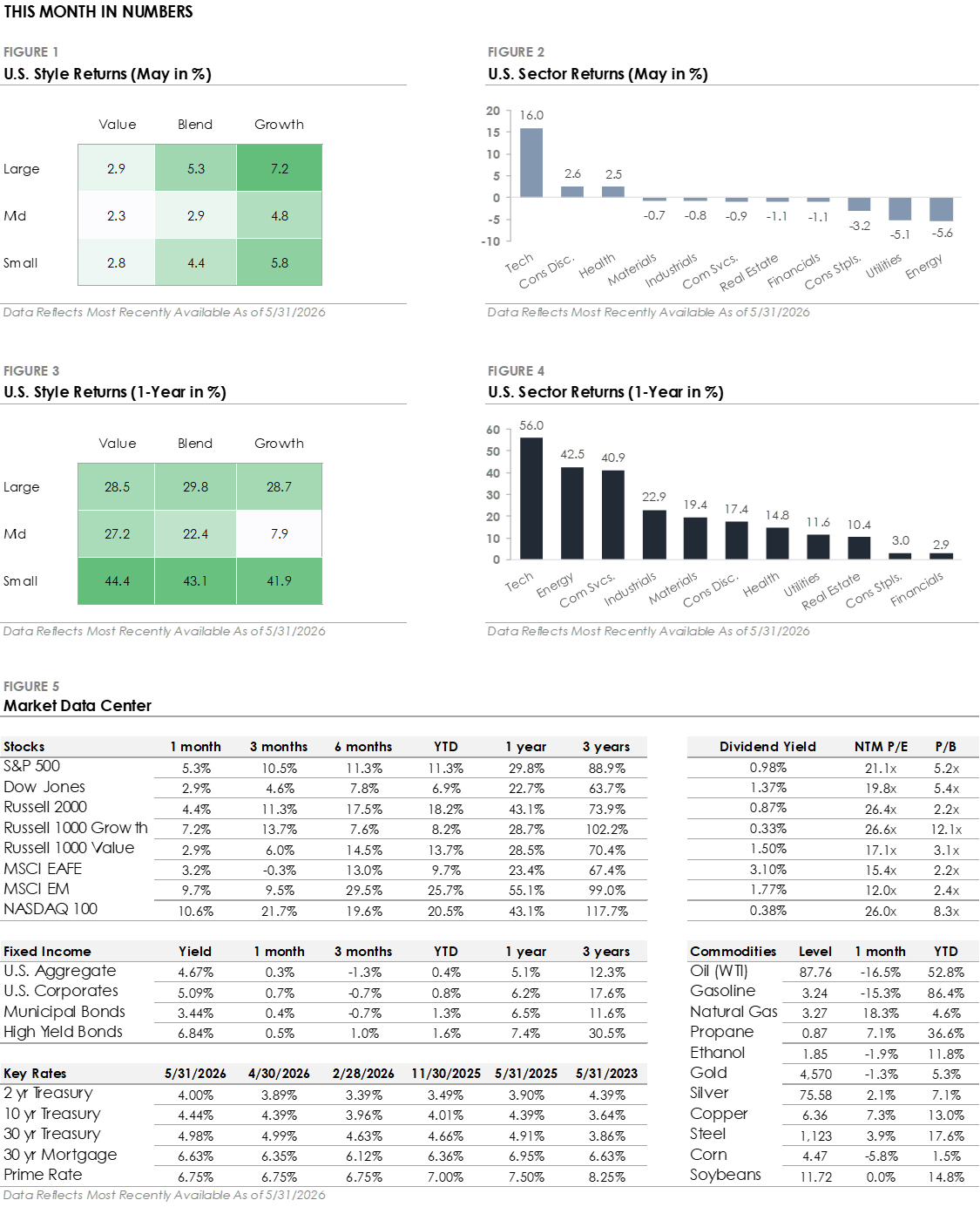

- The S&P 500 Index gained +5.3% in May and set multiple new all-time highs. Technology led all S&P 500 sectors with a +16.0% return, followed by Consumer Discretionary (+2.6%) and Health Care (+2.5%). However, eight of eleven sectors traded lower, led by Energy (-5.6%), Utilities (-5.1%), and Consumer Staples (-3.2%).

- Bonds traded higher despite a mid-month surge in Treasury yields. The U.S. Bond Aggregate returned +0.3% but underperformed corporate bonds as credit spreads tightened. Investment-grade and high-yield corporates returned +0.7% and +0.5%, respectively, with both outperforming the broader Bond Aggregate.

- International stock traded higher in May but were mixed. Emerging markets gained +9.7% and outperformed the S&P 500, while developed markets' +3.2% return lagged both U.S stocks and emerging markets.

Stocks Set New Highs as Geopolitical Tensions Ease

May was a strong month for equities, with most major indexes setting fresh all-time highs. The S&P 500 and tech-heavy Nasdaq 100 set new highs each week, with the Dow Jones and Russell 2000 also setting new highs throughout the month. Even the equal-weight S&P 500, which gives each company the same weight regardless of market cap, set a new high. While the equal-weighted index's move signals broadening participation, leadership was narrow within the index. The technology sector gained +16% and was the only sector to outperform the S&P 500 Index. Eight of eleven S&P 500 sectors traded lower, and ten of eleven sectors underperformed the index. The concentration showed up in factor indexes as well, with large-cap growth returning +7.2% versus +2.9% for large-cap value. The performance gap highlights a notable trend this year: AI and tech stocks continue to outperform more traditional, cyclical companies.

Bonds also traded higher, with the U.S. Aggregate Bond Index returning +0.3% and corporate bonds outperforming as credit spreads tightened further. The bond market’s gains came despite a surge in interest rates mid-month. The 30-year Treasury yield spiked above 5%, reaching levels last seen in 2007, and the 10-year Treasury set a new 52-week high. The trigger was back-to-back hot inflation reports for consumer and producer prices, with the Middle East conflict and elevated oil prices creating broader price pressures. Following the inflation reports, the market now places a greater than 50% probability of a Fed rate hike at the December 2026 meeting, a significant shift from earlier in the year when the market assumed a rate-cutting path. With Treasury yields at multi-decade highs and oil prices leading to inflation concerns, the bond market is shifting toward interest rates remaining higher for longer.

This Year’s Two Defining Themes: Geopolitics & Artificial Intelligencee Tech Sector

Two themes have defined markets this year. The first is geopolitics. Trade and tariff uncertainty earlier in the year has given way to military conflict in the Middle East, which has created an oil supply disruption. The Strait of Hormuz, which carries roughly 20% of global oil supply, has been effectively closed since the conflict began in late February, causing global oil inventories to shrink. Oil prices remain elevated after briefly hitting four-year highs earlier this year but have been relatively contained given the extent of the oil supply disruption. There was partial relief in May as U.S.-Iran negotiations progressed and the market began pricing in a potential reopening of the Strait. West Texas Intermediate crude ended the month below $90 per barrel, down -16.5%. However, the path forward remains uncertain, as a successful deal would take months to restore shipping traffic to pre-conflict levels. What happens next in the Middle East will impact energy prices, the inflation outlook, and the broader financial market.

The second theme is the artificial intelligence buildout. Companies have committed hundreds of billions to build the AI industry's physical backbone, including data centers, computer chips, and power generation. Forecasted 2026 capital spending across the leading tech companies now exceeds $600 billion, with most of the capex directed at AI infrastructure. The spending is driving economic growth and starting to show up in corporate earnings, with AI-linked revenue growth becoming a significant driver of overall S&P 500 profit growth. The investment is also creating drastic changes. Shortages across parts of the technology supply chains are creating bottlenecks, and companies are experiencing rapid growth as they repurpose products and services for the age of AI. The pace of spending and technological change explains much of the performance gap between the tech sector and more traditional areas of the stock market.

Firm Disclosures

The information provided herein is for general informational purposes only and is intended for your personal use and should not be circulated to any other person without our permission and any use, distribution, or duplication by anyone other than the recipient is prohibited. No portion of this commentary is to be construed as an offer or solicitation to buy or sell a security, or the rendering of personalized investment advice. The views and strategies described herein may not be suitable for all investors and are subject to investment risks. The content is developed from sources believed to be providing accurate information. The information contained herein should not be relied upon in isolation for the purpose of making any investment decision.

We believe the information contained in this material to be reliable and have sought to take reasonable care in its preparation and conducted reasonable due diligence to ensure the third parties’ performance is not materially inflated or incorrect; however, we do not represent or warrant its accuracy, reliability, or completeness, or accept any liability for any loss or damage (whether direct or indirect) arising out of the use of all or any part of this material. We do not make any representation or warranty regarding any computations, graphs, tables, diagrams, or commentary in this material which are provided for illustration/ reference purposes only. These views, opinions, estimates, and strategies expressed in it constitute our judgement based on current market conditions and are subject to change without notice. Any projected results and risks are based solely on hypothetical examples cited, and actual results and risks will vary depending on specific circumstances. Investors may get back less than they invested, and past performance is not a reliable indicator of future results.

Data which may be found in this document is based on our research and should not be taken as a forecast or an estimate of likely future returns. Any reference to a market index is included for illustrative purposes only, as an index is not a security in which an investment can be made.

Investments involve some sort of risk including potential loss of principal; diversification alone cannot guarantee against loss. Any projected results and risks are based solely on hypothetical examples depicted. Forward-looking statements should not be considered guarantees or predictions of future events. More complete information is available, including product profiles, which discuss risks, benefits, liquidity, and other matters of interest. The value of any investment may fluctuate as a result of market changes. Past performance is no guarantee of future results, and there can be no assurance the investment strategies discussed herein will prove profitable.

All opinions, estimates, investment strategies and views expressed in this document are subject to change without notice information. The recommendations made for your customized portfolio may differ from any asset allocation or strategies outlined in this document. Benchmark Financial does not guarantee the future performance of any portfolio, guarantee any specific level of performance, or guarantee any strategy or overall management will be successful or that the client’s investment objectives will be met.

Benchmark Financial is not a broker dealer and does not offer tax or legal advice. Please consult your tax or legal advisor for assistance regarding your individual situation. Investment Advisory Services offered through Benchmark Financial Wealth Advisors LLC, an SEC Registered Investment Advisor. Insurance services offered through Benchmark Financial Insurance LLC. The Benchmark Financial Wealth Advisors ADV Form 2A, 2B & Form CRS, which describe the services offered, fees charged and any conflicts of interest, are available upon request or online at www.bfllc.com. Additional information about Benchmark Financial and our advisors is also available online at https://adviserinfo.sec.gov/firm/summary/287966.